You've probably seen ads or heard friends talk about protecting retirement savings with gold. Maybe you're worried about inflation, market crashes, or just want something real backing your future. That's where companies like Augusta Precious Metals come in. But before you hand over your hard-earned money, you deserve to know exactly what you're getting into. This review cuts through the noise and tells you-plain and simple-how Augusta works, what's good, what's not, and whether it fits your situation.

What Exactly Is Augusta Precious Metals?

Augusta isn't a bank, a brokerage, or a flashy trading platform. It's a specialized firm that helps people buy physical gold, silver, platinum, and palladium for self-directed retirement accounts. They've been doing this since 2012 from their office in Beverly Hills, California. Their whole focus is on making precious metals accessible for long-term investors-not day traders or collectors.

One thing you'll notice right away: they don't try to sell you rare coins or fancy collectibles. Everything they offer must meet strict IRS rules for inclusion in a retirement account. That means high-purity bullion only-coins and bars that are at least 99.5% pure. If it doesn't qualify for an IRA, Augusta won't touch it. This isn't about hype or rarity; it's about compliance and real value you can actually use in your retirement plan.

How the Process Actually Works

Here's how things go when you reach out to Augusta. First, you'll talk to a representative-no online forms, no chatbots. This person walks you through how a precious metals IRA functions, what your options are, and whether it makes sense for your goals. There's no obligation to buy anything during this call. In fact, many people say their first conversation lasted 30 minutes or more, just answering questions without any pressure.

If you decide to move forward, Augusta connects you with an IRS-approved custodian. This is a third-party company that legally holds your retirement assets. You can't hold the gold yourself and keep the tax benefits-that's a hard IRS rule. Once your account is open, you choose which metals to buy. Augusta sends your order to a secure, insured depository like the Delaware Depository or Brink's. Your metals sit there safely, under your name, but you can't take them home.

You own them. They're yours. But they stay locked away until you retire or decide to take a distribution. The whole point is to keep your investment protected, both physically and legally, so it can grow quietly in the background while you focus on your life.

What Can You Actually Buy?

Augusta keeps their product list focused and compliant. You won't find obscure coins or overpriced "limited editions." Instead, you get widely recognized, liquid bullion such as:

- American Gold Eagle coins (22-karat, but IRS-approved thanks to their legal tender status)

- Canadian Gold Maple Leaf coins (99.99% pure, among the purest in the world)

- American Silver Eagle coins (the most popular silver bullion coin in the U.S.)

- Australian Kangaroo gold coins (also known as Nuggets, highly trusted globally)

- 1-ounce gold and silver bars from trusted refiners like PAMP Suisse, Valcambi, or Heraeus

Every item comes with full documentation and meets the purity standards the IRS requires. That's non-negotiable. Augusta won't offer anything that could jeopardize your IRA status, even if it's more profitable for them. That kind of discipline builds trust over time.

Real Advantages of Choosing Augusta

After talking to dozens of customers and reviewing their materials, several strengths stand out clearly:

- Education over sales. Their reps spend time explaining market trends, tax rules, and risks-not just pushing products. You'll learn why gold matters in uncertain times, not just how to buy it.

- All-in pricing. You see the current metal price, the markup, and the total cost before you commit. No surprise fees later. Transparency like this is rare in the financial world.

- Free delivery to vaults. Shipping and insurance to the depository cost you nothing. That's a real savings, especially when you're buying tens of thousands of dollars' worth of metal.

- Ongoing support. Even years after your purchase, you can call with questions about your holdings or the market. They don't disappear after the sale.

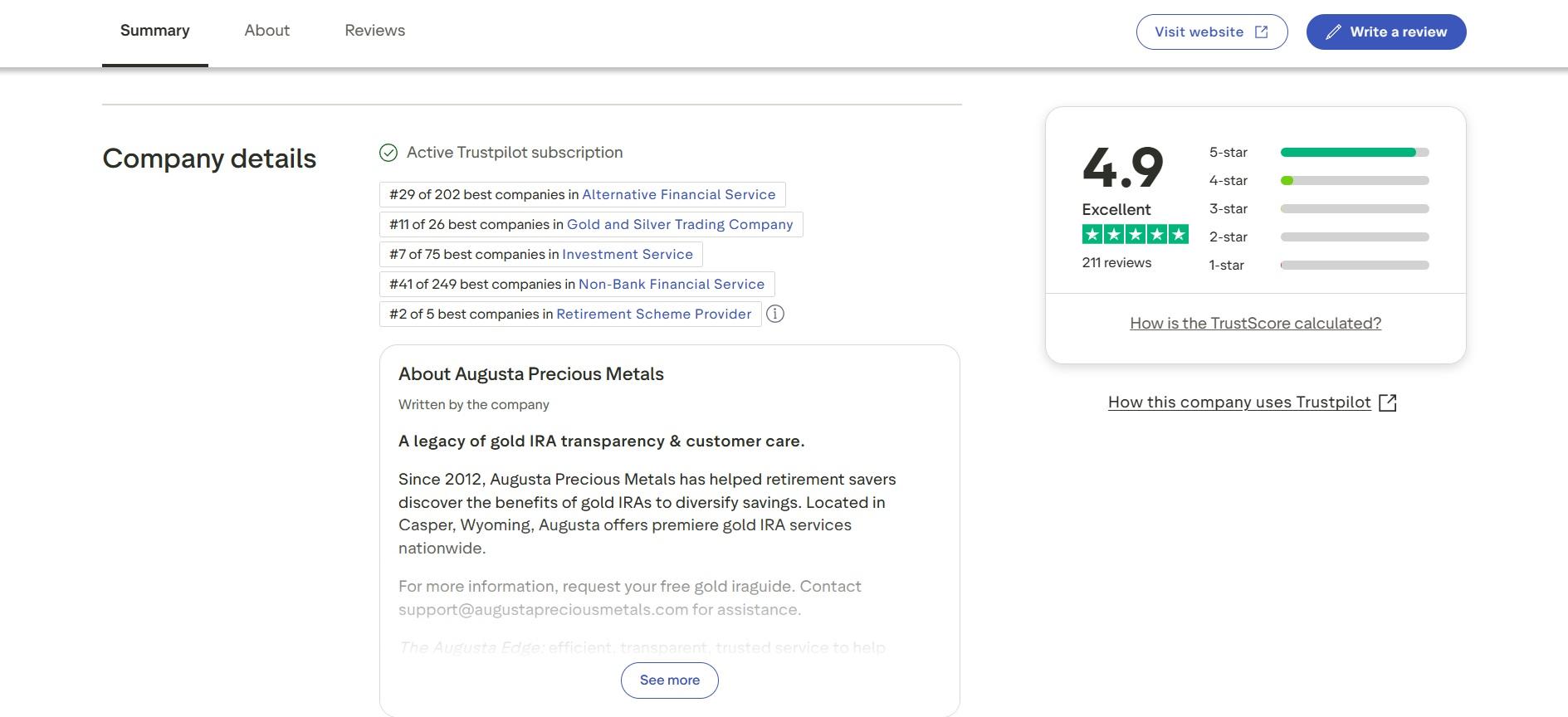

- Strong track record. They hold an A+ rating with the Better Business Bureau and have thousands of verified positive reviews across Trustpilot, ConsumerAffairs, and other platforms.

Many people say they felt respected during the process-like they were making an informed choice, not being pressured into a quick sale. One teacher nearing retirement told us, "I called three companies. Augusta was the only one that didn't make me feel dumb for asking basic questions."

Where Augusta Falls Short

No service is perfect, and Augusta has limitations you should know about:

- High entry point. You need $50,000 to open a new precious metals IRA. That's out of reach for many savers, especially younger investors or those just starting to build retirement funds.

- No online dashboard. Everything happens over the phone. If you like managing accounts digitally, checking balances instantly, or placing orders with a click, this feels old-fashioned-even frustrating.

- No physical delivery option for IRAs. You can't have the metals shipped to your house if they're in a retirement account. (You can buy outside an IRA for delivery, but that's a different process with different tax implications.)

- Annual storage fees. The depository charges you each year to keep your metals safe-usually between $100 and $300, depending on the size of your holdings. It's a small price for security, but it adds up over decades.

These aren't hidden traps-they're just part of how the system works. But they matter if you're on a tight budget or prefer hands-on control. Augusta isn't trying to hide these facts; they explain them upfront. Still, they're worth weighing carefully.

What Customers Really Say

Most reviews highlight the same things: patience, clarity, and professionalism. People appreciate that reps don't rush them. One retiree said, "They explained gold like I was smart but new to it-not like I needed to be sold to." Another customer, a small business owner, mentioned how helpful it was to get a clear breakdown of fees before signing anything.

Complaints are rare but usually involve wait times during busy periods (like when gold prices jump suddenly due to global events). Others mention the $50,000 minimum as a barrier. But very few accuse Augusta of misleading them or hiding costs. That consistency builds credibility in an industry full of flashy promises.

That trust matters. When you're buying something you can't see or touch, knowing your provider is honest makes a huge difference. Augusta seems to understand that long-term relationships beat quick commissions.

Who Should (and Shouldn't) Use Augusta

Augusta makes the most sense if you:

- Have significant retirement savings to diversify-typically $50,000 or more

- Want physical, IRS-compliant bullion-not collectibles or speculative items

- Prefer personal guidance over digital self-service

- Are thinking in decades, not days

- Value peace of mind more than the lowest possible price

It's probably not the best fit if you:

- Have less than $50,000 to invest

- Want to hold gold at home in a safe or safety deposit box

- Prefer managing everything through an app or online portal

- Are looking for short-term speculation or quick profits

- Need ultra-low fees above all else

There's no shame in either path. It just depends on your goals, your budget, and how you like to manage your money. Augusta isn't for everyone-but for the right person, it's a solid partner.

Bottom Line

Augusta Precious Metals won't dazzle you with tech or ultra-low prices. What they offer is something rarer these days: consistency, transparency, and respect for your intelligence. They assume you're serious about protecting your future-not chasing hype or gambling on market swings.

Yes, the $50,000 minimum is steep. Yes, you have to talk on the phone. But if you value clarity over convenience and long-term security over quick clicks, Augusta stands out in a crowded field. They've built a business on doing one thing well: helping people add real, physical assets to their retirement without gimmicks.

Before you decide, do this: call them. Ask tough questions. See how they answer. A good company welcomes skepticism. Augusta has built its reputation on that principle and so far, they've earned it. Whether or not you end up investing with them, you'll walk away better informed. And in today's financial world, that's worth its weight in gold.